Financial Statements contains from 5 financial statement. The primary goal of financial accounting is the preparation of financial reports.

For the purpose of clarifying the financial position and profitability of the company on a specific date and providing useful financial information to the users , whether inside or outside the establishment.

the establishment represent a structural presentation of the financial nature of its financial position and the transactions it has completed.

Generally, financial statements aim to provide information about the financial position, activity results and cash flows that benefit a wide range of users in decision-making and help to show the results of the administration’s use of the available resources.

To achieve this objective, the financial statements provide data on the following:

Assets,

Liabilities,

Equity,

Revenues and expenses including profits and losses,

Other changes in equity and

Cash Flow.

This information – in addition to other information contained in the notes supplementing the financial statements – helps the users of the financial statements in forecasting the future cash flows of the establishment, especially the timing and likelihood of generating these cash flows.

To achieve this goal, the International Accounting Standard No. 1 “Presentation of Financial Statements“ defined the general considerations for presenting the financial statements and provided an explanation of their structure and the minimum components of the required financial statements. And the income statement, as well as in the presentation of the statement of changes in equity.

So that the integrated financial statements must include the following components:

Balance Sheet

Income Statement

Changes in Equity Statement.

Cash Flow Statement.

Supplementary Notes, including a summary of the most important accounting policies and any other explanatory notes.

Documents required to start preparing financial statements:

Accounting Cycle – Financial Statement

Preparing financial statements

Recording in the journal based on the evidence, supporting the occurrence of the financial process.

Posting from the Journal record to the ledger record, and the trial balance.

Preparing the trial balance of totals and balances.

Preparing the closing entries in the journal record and migrating them to the ledger to show the results of the final accounts.

Functions of financial statements:

Measure the assets that fall into the ownership of the company.

Measuring the obligations arising from the rights owned by the company (which are liabilities and the rights of capital owners).

Measuring the changes that occur to those assets, liabilities and the rights of capital owners.

Linking these changes to specific time periods.

Classification of the changes referred to as follows:

Revenues, expenses, gains, and losses.

Other changes in assets, liabilities, and capital rights.

Expressing the above in monetary units, as it is the general unit of financial measurement.

Preparing financial statements and periodic reports on the company’s assets, liabilities, rights of capital owners at a specific point in time, net income, and parts thereof, and cash flows during a certain period of time.

Process audit: This type of audit verifies that processes are working within established limits. It evaluates an operation or method against predetermined instructions or standards to measure conformance to these standards and the effectiveness of the instructions

The general model of the audit process consists of the following basic stages:

– Client acceptance.

– Planning the audit process.

– Tests and audit guides.

– Evaluation and release of the report.

A. Definition of auditing Definition

Auditing of accounts means examining the internal control systems, data, documents, accounts, and notebooks of the project under scrutiny, with a systematic critical examination, with the intention of coming up with a neutral technical opinion about the extent of the significance of the financial statements about the financial position of that project at the end of a known period of time, and the extent to which they portray the results of its work in terms of profit or loss during that period.

Thus, the audit process includes Examination, Verification, and Reporting.

Examination and Verification

The examination is intended to ensure the correctness and integrity of the measurement of the operations that have been recorded, analyzed, and classified, that is, an examination of the mathematical measurement of the financial operations of the specific activity of the project.

As for the Verification, it is intended to judge the validity of the final financial statements as a valid expression of the project’s business for a specific financial period, and as an indication of its financial position at the end of that period.

Thus, examination and verification are two interrelated functions intended to enable the auditor to express his opinion on whether the measurement processes of financial transactions have led to establishing a fair picture of the outcome of the project’s work and its financial position.

As for the report, it is intended to crystallize the results of the examination and verification and prove them in a report presented to those who are interested in the matter inside and outside the entity, which is the conclusion of the audit process, in which the auditor expresses his / her neutral technical opinion on the financial statements as a whole in terms of their portrayal of the project’s financial position and its operations in a sound and fair manner.

The expression “Fair Presentation” means the data contained in the financial statements are consistent with the reality of the project, and this requires these data to be accountably sound and adequate, meaning that nothing has been omitted and that the auditor certifies all of this.

In general, the objectives of the audit can be limited to several aspects, the most important of which are:

1- Ensuring the accuracy and correctness of the accounting data recorded in the books and records of the project and determining the extent of reliance on them.

2-Obtaining an impartial technical opinion on conforming the financial statements to what is recorded in the books and records.

3- Discovery of errors or fraud that may exist in the books.

4- Reducing the chances of errors and fraud through sudden auditor visits to the project and strengthening the internal control systems used by him.

Auditing Goals

Today, the audit process has diversified these goals into other goals and purposes, the most important of which are:

Monitoring the established plans and following up on their implementation.

Evaluating the results of the project work in relation to the set objectives.

Achieving the maximum possible production efficiency by eliminating wastefulness in all aspects of the project’s activity.

B. Types of audit

There are several types of auditing that differ according to the angle through which the audit is viewed. But the performance levels that govern all types are the same. In general, the audit categorizes – according to different points

of view – into the following:

What follows from this chapter is an explanation of all these different types.

The audit in terms of the Scope of Audit

Complete audit: here, the auditor examines the entries, documents, and records with the intention of reaching a neutral technical opinion on the validity of the financial statements as a whole.

This type was fully scrutinized in detail (Detailed Audit).

The auditor examines any restrictions and the other 100% were on the projects audited accounts are small in size and its operations are few in number. This has turned into a (test Check audit).

As a result of the development that occurred in the business world and the accompanying emergence of large industries and joint-stock companies, so that it did not become reasonable for the auditor to audit all operations, records, and documents.

The adoption of the sample and test method in auditing increased the projects’ interest in internal control systems. Because the number of tests and the size of samples depends on the degree of robustness of those systems used, the auditor increases the percentage of his tests if these systems are weak and there are gaps in them.

Thus, it becomes clear that the difference between these two types of audits lies in the difference in the scope of the audit process only. The authority of the auditor in both types cannot be limited in any way, as he alone has the right to decide the scope of the audit process.

Partial audit:Here, the auditor’s work is limited to some operations and items without others, such as being entrusted with checking cash-only, or inventory… etc. In this case, he/she cannot come up with an opinion on the financial statements as a whole, but the auditor’s report is limited to what has been identified for him/her of the issues.

It is desirable here for the auditor to obtain a written contract that clarifies the scope of the audit process entrusted to him so that he is not accused of negligence or failure to perform the audit of a clause that he was not originally entrusted with auditing, thus protecting himself through the contract from any such responsibilities.

The audit is in terms of the Timing of the Audit.

Final audit:

The auditor is assigned to carry out such an audit after the end of the financial period to be audited because the accounts have been closed in advance, and it is a feature of this type of audit that it is blamed for:

His / Her failure to discover what is on the books of errors or fraud if they occur.

Taking a long time may lead to the report being submitted on time.

Confusion to work in both the auditor’s office and the client, as the bookkeeping dates coincide in many client projects for the same office, which leads to the sacrifice of some accuracy in performance in exchange for speeding up the work, in addition to that the work may stop for some time until the auditor collects evidence and the necessary clues.

It is clear that this type is suitable for application in small or medium enterprises and is limited in most cases to fully and detailed auditing of the elements of the financial statements, especially the budget, and for this reason it is often called the budget audit.

Continuous auditing:

Here the auditor checks the accounts and documents on an ongoing basis, as he makes multiple visits to the facility subject of auditing throughout the period he audits, and then at the end of the year audits the final accounts and the budget. It is clear that this type is suitable for auditing large establishments, as it is difficult to audit them through a final audit.

This type of audit has the following characteristics:

The auditor has sufficient time to enable him to get to know the establishment better and to audit more fully.

Rapid detection of fraud and error in a short time instead of leaving it until the end of the year.

The regularity of work in the auditor’s office and in the project as well, due to the wide scope of time for auditing.

Reducing the chances of tampering with the books because of the psychological impact of repeated visits by the auditor on the project staff.

The completion of the work on time without negligence or delay by the project staff, due to the auditor’s hesitation in the facility as well.

But despite these advantages, the constant scrutiny of the following blames:

The possibility of the establishment employees changing or deleting numbers or entries in documents and records after checking them, whether in good faith or with intent to cheat to cover embezzlement, depending on the fact that the auditor does not return again to audit those documents and records.

Here, the auditor can avoid this occurrence by placing certain signs or symbols in front of the data or account balances that he audited and verify their validity, or by taking a note of the account balances that he finished auditing until the date of the audit.

Suspending the work of the employees of the accounts department from time to time when visiting the auditor to check what has been proven in the books and records, but he can overcome this by his good choice for the periods in which he visits the facility.

The possibility of the auditor neglecting to complete some of the things he left open on his last visit. However, he can overcome this by referring to his observations, in addition to the existence of an audit program in which the auditor confirms the work that has been accomplished step by step.

The possibility of acquaintance and friendship links between the auditor and the project’s employees due to his frequent reluctance to the project, which causes embarrassment to the auditor when he discovers fraud or error in the project books, or when writing the report.

The potential for this ongoing audit process to turn into a chore.

However, the auditor can avoid this by introducing modifications in the audit program, which must be flexible.

The audit is in terms of the Staff of Audit.

Internal Auditing:

This audit is carried out by an internal body or auditors affiliated with the facility, in order to protect the facility’s funds and to achieve management objectives such as achieving the greatest possible administrative and productive efficiency for the project and encouraging adherence to administrative policies.

External audit:

its main purpose is to conclude a report on the fairness of the general budget portrayal of the company’s financial position and the fairness of portraying the final accounts of the results of its business for the relevant financial period. Therefore, it is carried out by a neutral external person independent of project management. That is why this type is sometimes called a neutral or independent audit.

It should not be borne in mind that the existence of a sound system of internal auditing obviates the auditing of accounts by an independent external auditor, because of the above differences between the two types, the most important of which is the lack of neutrality in internal auditing because the internal auditor is subordinate to the administration that serves its objectives, while the principle of independence in external audit Where the auditor here is a remunerated agent for the majority of the shareholders or the owners of the project.

Audit in terms of the Degree of Compulsion

Mandatory auditing:

This is the audit that the law stipulated that must be carried out. Then the penalty can be imposed on companies that fail to do so and do not provide Reports of their final accounts and financial positions audited by licensed account auditors. This type is sometimes referred to as legal audit Statutory Audit It is not true that this should be fully scrutinized.

Optional audit:

which is required by the establishment’s owners without a legal obligation to do so. This is the case for individual projects, LLC, and joint ventures), and this may be fully or partially according to the desire of the establishment owners and as indicated in the contract concluded between the auditor and the client.

The audit was first optional, and a long period of time passed until it became legally binding when the minds of those in charge of the economy generated the need to respect the provision of the neutral external account audit component, and to include it in the statutory company contracts the provisions related to this aspect.

For whom is interested to be an auditor:

C. Definition of auditor:

An auditor is a person who possesses the required academic and practical qualifications and who takes the work of accounting and auditing a regular profession that he practices after obtaining a license to do so from the official authority in the state. In the USA, AICPA is the association responsible for certifying the external auditors.

D. The scientific and practical qualification of the auditor

The auditor must have scientific competence as well as practical competence in addition to his knowledge.

Most of the countries in the world have stipulated the availability of the following academic qualifications in the auditor, namely: Obtaining, as a minimum, a bachelor’s degree in commerce (accounting major) or one of the academic degrees in commercial, financial, or economic sciences whose study programs include accounting materials in order to gain the auditor’s familiarity and knowledge of all types and branches of accounting.

E. Personal characteristics and the basis of professional behavior of the auditor:

1- Personal characteristics:

The most prominent universally recognized qualities in the personality of an auditor are:

Skill and great caution in carrying out his work and estimating the responsibility entrusted to him/her.

To be honest, impartial, and fair during the exercise of his work.

To be secretive and trustworthy, keeping the secrets of the projects whose accounts, he audits, and not to use the secrets obtained for the benefit of any other institution.

He should be endowed with perseverance and brave work and say the truth in his reports without favoritism.

2- The foundations of professional conduct:

Members of the profession adhere to fair competition among themselves, and they are not entitled to resort to advertising or propaganda, or to enter into wage tenders, or to pay commission in exchange for a job.

That the wage is commensurate with the effort, it is not permissible to accept low wages that are not commensurate with the effort made to compete with another colleague by accepting a wage less than what he would receive.

When there are multiple auditors in a single project, they must cooperate and divide the work between them in a way that secures the public interest.

Not accepting the engagement with a job with any project weakens the objectivity of providing professional services and his role as one of those responsible for strengthening and improving the profession.

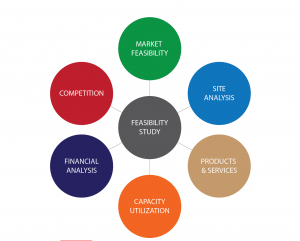

The feasibility study is an integrated set of specialized studies that are carried out to determine the validity of the investment in all its aspects, so some search for how to prepare a feasibility study, to predict knowledge of the possibilities and failure of the project.

Knowing the extent to which your project was feasible or, and is it worth making this investment, the feasibility study shows the likelihood of success of this project and the possibility of failure, and if it turns out that this project or idea overcomes the loss, in that it is excluded, but in the case of clarification that the idea will succeed with great probability, the project is being prepared.

Therefore, when carrying out a feasibility study, a question must be asked whether the idea of the project is feasible or not, and that point should be clarified in all its aspects, whether the financial, technical, marketing, economic, social and legal aspects, all of which to ensure the achievement of the objectives specified in this project and to ensure its success.

This element includes knowledge of the extent of item properties and know the number of competitors in the neighboring area to be doing the project, and the possibility of selling the commodity.

In addition to determining the extent of its marketing share through which it can serve the study, it is the most important stage in the feasibility study in which the market is studied, and the following is identified through it.

– The size of the demand for the good or service provided by the project.

– The size of the offer of the item to be offered.

– Determine the volume of sales according to the size of supply and demand.

– determine the need and desire ups target customers.

– knowledge, products, and prices of competitors activity in the target market.

– identify opportunities and gaps that can be exploited for the project.

This study includes knowing the fixed assets required by the project, i.e., knowing all the mortal matters related to the project. My understanding is among the important elements that must be known when doing the search for how to prepare a feasibility study. There is no feasibility study without the technical study, so you must know and define the following.

– determine the location.

– Determine the area, specifications, and costs of the project headquarters.

– Determine the quality, specifications, and labor costs.

– Proportion of project costs in terms of tools, equipment, and supplies.

– Determining the costs and needs of the project in terms of services such as water, energy, and others.

In the case of productive projects, the need and costs of the project are determined in terms of production supplies and raw materials.

The financial study is one of the most dangerous stages of the feasibility study, because it is through it that the revenues and profits of the project must be identified. In this study, all financial resources allocated to the project, in addition to the project costs, are searched for, and to determine the total cost of the project, and the monthly and total profits of the project.

– Find out how much the entrepreneur needs to get started.

– Does the project need external funding?

– determine the pricing structure that will be used.

– How well the project could survive in the absence of sales.

– How long does the project need to achieve parity between sale and profit?

In order to know how to prepare a feasibility study, all of its elements, including technical feasibility, must be known, and it is one of the most important elements. You must respond and know all the following questions to ensure the success of the project.

What is the service or product on which the project is carried out?

Is this service or product already on sale? If the answer is no, what is the method or cost you need to bring it into the market?

How do you protect your product or service from competitors?

identify strengths and weaknesses of the product.

The materials you need to produce a product or service.

How well are you able to get the materials you need.

The social feasibility is based on a study determining the values that will be added to the project for the community, such as job opportunities, and whether this project is consistent with the values of the community, whether religious, cultural and heritage or not, in addition to assessing the effects of the project on the environment, whether positive or negative, in addition to the interest in reducing the percentage of damage that could harm the environment.

Choosing the type of service or commodity must be well taken care of, as it is one of the most important elements in the economic feasibility study, in addition to paying attention to the quality of service and the target group, as this step gives the extent of success or failure of this project.

Take well about an informed decision should how start operation of the project and determine the consequences that could arise during doing this project to determine whether it fits the surrounding community or not, Om da community can demand this either type of service or product.

Determining the project costs, through a detailed financial study that clarifies the fixed costs, such as rents, salaries, tax fees and insurances for the worker, insurances for the project, and depreciation, in addition to variable costs, which include the necessary raw materials and transportation, in addition to maintenance fees, electricity and water expenses.

A detailed description of the proposed project must be developed, which consists of the name of the project, its employers, the location in which the project is carried out, in addition to the legal form of the project, the proposed activities, and all project activities.

The size of the market, the volume of sales in it, the services that will be provided, the organization and qualification of a functional cadre for that, in addition to the appropriate distribution of tasks, the estimation of the project needs, and the determination of the target group for this project and the services that will be provided.